Should I Refinance My Auto Loan?

Get the steps and signals to make a confident refinance decision.

Published Monday, May 4, 2026 to Advice

Should I refinance my auto loan? It’s a common question drivers ask when rates go down, budgets get tighter, or credit scores improve.

Auto loan refinancing can lower your interest rate, reduce your monthly payment, or help you pay off your car sooner. But it isn’t the right move for everyone.

Understanding when refinancing works in your favor (and when it doesn’t) is the key to avoiding costly mistakes and maximizing potential savings.

Start at the beginning: auto loan refinancing guide >

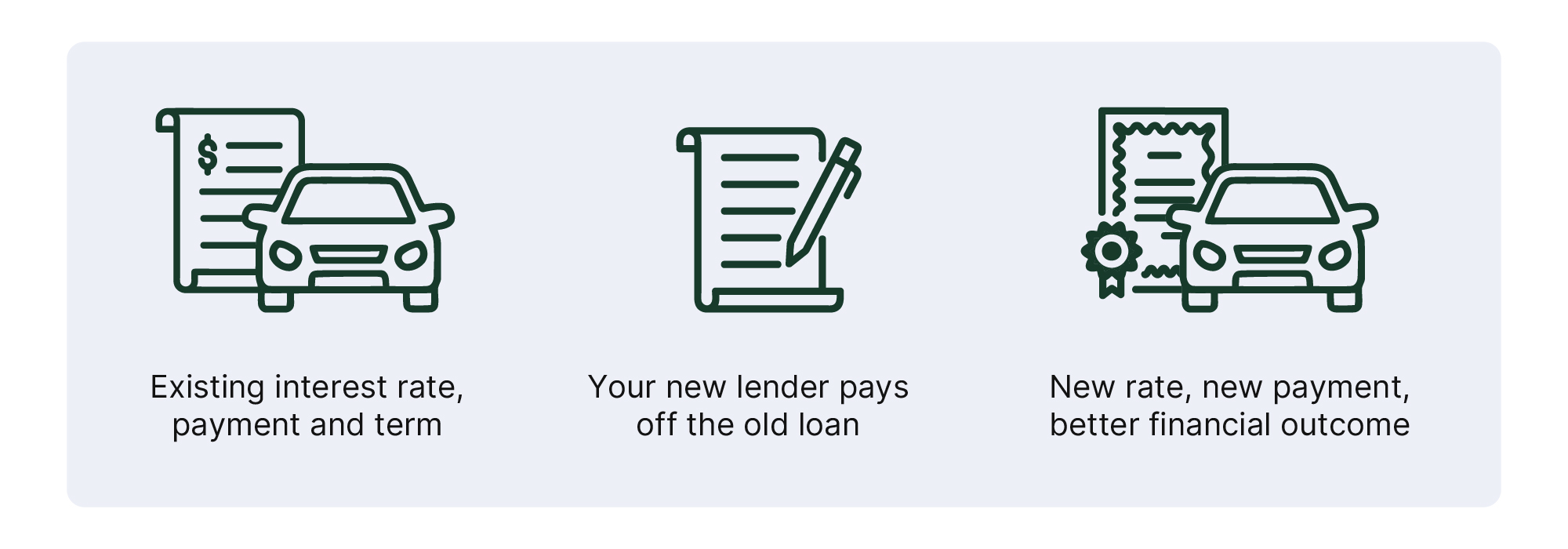

How Auto Loan Refinancing Works

Refinancing simply replaces your current auto loan with a new one, usually from a different lender. If you qualify for a lower interest rate than what you’re currently paying, you can reduce the cost of borrowing over the life of your loan.

Some borrowers refinance to shrink their monthly payment, while others refinance to shorten their loan term and pay off the car faster. The process is typically quick, paperwork is minimal, and most lenders allow refinancing within the first couple of months of ownership.

Signs You Should Refinance Your Auto Loan

1. Your interest rate is higher than today’s market rates

If interest rates have dropped since you bought your car, refinancing may help you secure a lower rate. Even a small rate reduction can create meaningful long-term savings, especially if you still have several years left on your loan.

2. Your credit score has improved

Your credit score heavily influences your auto loan rate. If your credit score has risen since you signed your original loan, you may now qualify for significantly better terms. Refinancing can help you capture those savings and reduce what you pay overall.

3. You need to lower your monthly payment

Life happens. Budgets shift, expenses grow, or income changes.

Refinancing into a longer loan term can ease short-term financial pressure by lowering your monthly payment. While extending your term may increase the total interest you pay, it can provide helpful breathing room when cash flow is tight.

4. You want to remove a co-borrower

If your financial situation has changed, refinancing can help you restructure who is responsible for the loan. For example, this is common when a parent wants to remove themselves from a loan originally taken out with their child.

When You Should Not Refinance Your Auto Loan

1. You owe more than your car’s value

If you owe more on your car than it’s worth (negative equity), refinancing may be difficult or may trap you into rolling excess debt into a new loan. That can extend repayment unnecessarily and increase interest costs.

2. Your car is older or has high mileage

Lenders typically have vehicle age and mileage requirements. If your car is older, has significant wear, or has depreciated rapidly, you may struggle to find favorable refinance terms.

3. You’re near the end of your loan term

If you’re close to paying off your car, refinancing might not save you enough to justify the effort. Most of the interest on auto loans is paid early in the term, so refinancing late often produces minimal benefit.

4. Fees outweigh the savings

Some lenders charge refinancing fees, and your current lender may charge a prepayment penalty (though this is rare for auto loans). If fees offset the savings from a lower rate, refinancing may not be worthwhile.

How to Know if Refinancing Will Save You Money

A simple way to evaluate your refinancing potential is to compare the interest you'll pay over the remaining life of your current loan versus the interest you'd pay on a refinanced loan with better terms. An auto refinance calculator can quickly show your potential monthly and long-term savings.

If the difference is meaningful and fees are low or nonexistent, refinancing is probably a smart move.

How Soon Can You Refinance an Auto Loan?

Most lenders allow refinancing as early as 30 to 60 days after you purchase your vehicle. As long as your title and loan account are fully set up, you can apply.

Does Refinancing Hurt Your Credit?

Refinancing typically triggers a hard credit pull, which may cause a small, temporary dip in your score. Once your new loan is active, maintaining on-time payments can help improve your score over time. Overall, the impact is minor for most borrowers.

Bottom Line: Should You Refinance Your Auto Loan?

Refinancing makes the most sense if you can secure a lower interest rate, reduce your monthly payment, or take advantage of improved credit. However, if your loan is nearly paid off, your car is old, or you owe more than your car is worth, refinancing may not deliver the results you expect.

If you’re considering your next steps, explore our auto loan refinance guide to compare rates, understand the full process, and determine the best refinancing strategy for your situation. Or you can learn more about auto loan refinancing at Veridian.