Auto Loan Refinancing: Your Path to Lower Payments

Learn how you can lower your monthly payments and pay less interest.

Published Monday, May 4, 2026 to Advice

Your car payment is a fixed expense. But that doesn't mean it's locked in forever.

If interest rates have dropped, your credit has improved, or your budget needs breathing room, an auto loan refinance could put money back in your pocket.

Still, many drivers hesitate because they’re unsure how the process works or even if they should refinance their auto loan at all. The good news is that refinancing is often simpler than people expect, and the savings can be significant when the timing is right.

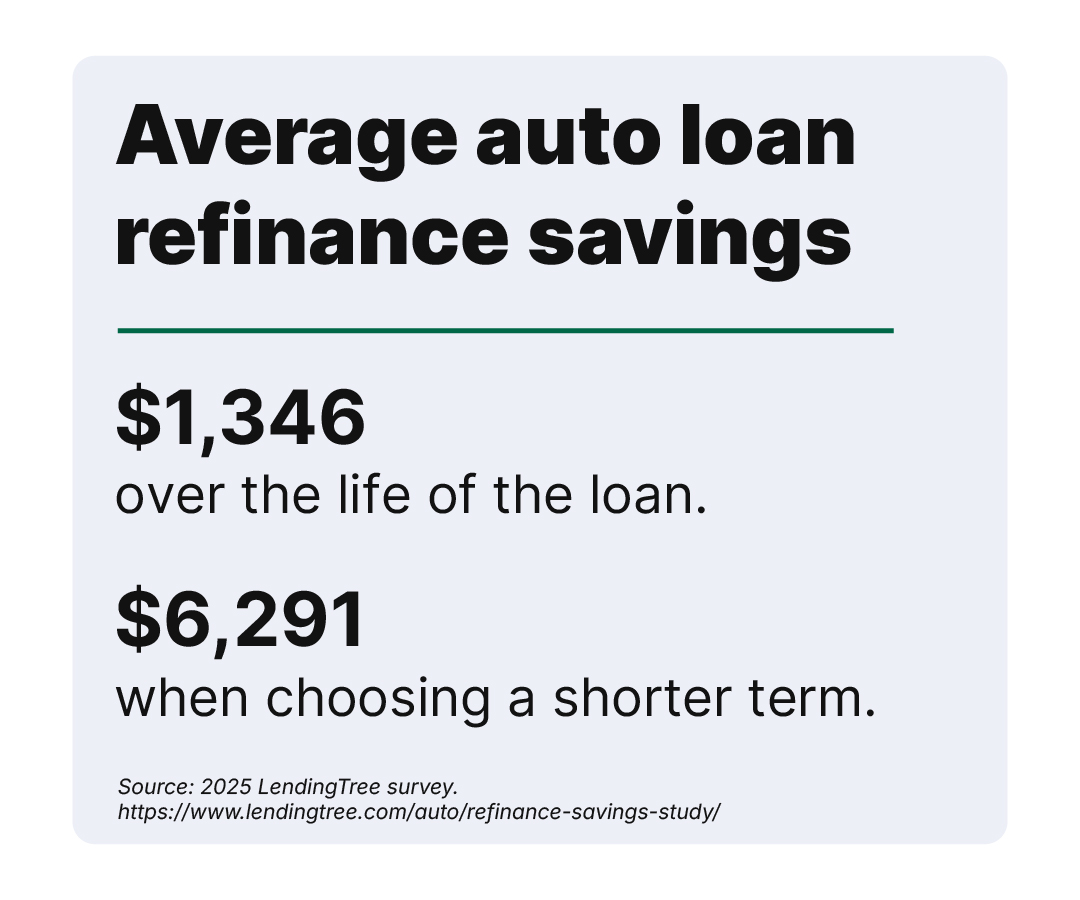

A 2025 LendingTree study showed that Americans who refinance their auto loan save an average of $1,346 over the life of their loan. Those who choose to shorten their term save even more: $6,291 on average.

In this guide, we’ll break down exactly what refinancing is, how to refinance an auto loan step by step, and how to decide whether it makes sense for your financial situation—so you can move forward with confidence, not guesswork.

What Is Auto Loan Refinancing?

Auto loan refinancing is simple: you take your current auto loan and move it into another auto loan, often with a better rate or term. In most cases, you will move your loan from your current financial institution to another.

There are a few main reasons you may consider auto loan refinancing:

- Lowering your monthly payments

- Reducing your interest rate and paying less interest over time

- Shortening your term to pay your loan off faster

Before you decide to refinance your auto loan, you should understand how the whole process works. Let’s get into it.

How Auto Loan Refinancing Works

The process of auto loan refinancing is very simple. The bank or credit union you’re applying with should do most of the heavy lifting.

You’ll start by submitting your application. Then, the financial institution you’re applying with will start the background work, like:

- Reviewing your credit

- Valuing your vehicle to ensure it’s not worth less than the amount you’re borrowing

- Calculating the payoff amount to your current loan servicer

Once you’re approved for your auto loan refinance, your new loan servicer will pay off your existing loan and replace it with the new one. It’s that simple.

In many cases, the whole process can be completed in just a few days, but can take up to a few weeks to work things out between your current and new financial institutions.

How to Refinance an Auto Loan: Step-by-Step

Auto loan refinancing doesn’t start with the application. It starts with doing your research to ensure you’ll benefit from it.

Here’s a step-by-step guide to auto loan refinancing.

Step 1: Review Your Current Loan

Make sure you understand the details of your current loan, including:

- Interest rate

- Remaining term

- Your remaining balance

- Payoff amount

It’s worth noting that your payoff amount could be different from your remaining balance to cover final interest charges or early payoff fees.

Step 2: Check Your Credit and Financial Situation

If your credit has improved since you bought your vehicle and got your current auto loan, you’re more likely to be offered a better rate. If your credit hasn’t improved much, it may not be the right time for auto loan refinancing.

Step 3: Compare Refinance Offers

If you have a financial institution you love and want to refinance with them no matter what, that’s great. But, in most cases, you’ll want to shop around to compare auto loan refinancing offers.

Be sure to look at:

- APR*

- Terms

- Fees

- Special offers, like cash back

Step 4: Submit Your Application

Now it’s time to submit the application. When applying, you may be asked for some or all the following information:

- Your ID

- Proof of income (pay stubs, W-2s, etc.)

- Vehicle information, like the year, make and model, mileage, and your Vehicle Identification Number (VIN)

- Current loan information, including your current lender, account number and 10-day payoff amount

- Proof of insurance showing comprehensive and collision coverage

This may not be a comprehensive list of the documents you need. Check with the financial institution when you’re applying for a full list.

Step 5: Finalize the New Loan

Once you’ve submitted your application and it’s been approved, your new loan servicer will handle the transition. They’ll pay off the old loan and get your new loan set up.

The new servicer will let you know when your new auto loan is ready to view and manage on their digital banking platform. You’ll most likely also receive documents in the mail or in-person at a branch.

Should I Refinance My Auto Loan? Key Questions to Ask

Question 1: Is my interest rate high? If your interest rate is higher than what you’re seeing promoted, auto loan refinancing may be a good option.

Question 2: Has my credit score improved? A better credit score can help you qualify for better rates and terms.

Question 3: Do I need to free up my budget with lower payments? If you have other goals, you’re working toward, auto loan refinancing can help you get there.

Question 4: Do I want to pay off debt faster? Auto loan refinancing can help you lower payments to free up more money to put towards paying off other, higher-interest loans.

Learn more: how auto loan refinance fits into your debt reduction strategy >

Question 5: Am I going to keep driving this vehicle for a while? If you plan on shopping for a new car soon, you may not want to consider auto loan refinancing. And older vehicles may not qualify.

Consider all the details when determining if you should refinance your auto loan >

Benefits of Auto Loan Refinance

There are several benefits of auto loan refinancing. Here are a few of the most popular:

- Lower monthly payments for immediate budget relief

- Lower interest costs over the life of the loan

- Shorter loan terms for faster payoff

- Flexibility for improving your financial plan

These advantages and more are why so many drivers explore lowering their car payment with auto loan refinance.

Read more about all the benefits of auto loan refinance >

When Auto Loan Refinancing May Not Be the Best Fit

Refinancing can deliver real savings, but it isn’t the right move for everyone. Here are situations where an auto loan refinance may not work in your favor:

Your vehicle is too old or has high mileage.

Lenders often set limits on model year and mileage, and older vehicles can fall outside those guidelines. If your car has significant wear, you may have fewer refinance options—or none at all.

You owe more than the car is worth.

Most lenders typically won’t approve a loan that exceeds the vehicle’s value. Even if you’re approved, the numbers may not improve your financial position.

Your current loan has prepayment penalties.

Some lenders charge fees for paying off your loan early. If these costs outweigh the potential savings, refinancing may not provide a net benefit.

Your credit hasn’t improved or interest rates haven’t dropped.

Refinancing works best when you can qualify for a lower rate. If market rates or your credit profile haven’t changed, you’re unlikely to see better terms.

You’re planning to sell the vehicle soon.

If you expect to trade or sell your car soon, refinancing may not give you enough time to recoup the benefits of a lower APR or new term.

How to Compare and Find the Best Auto Refinance Rates

Finding the best auto refinance rates starts with comparing offers. Rates can vary between lenders, and even small APR* differences can lead to meaningful long term savings.

Start by checking rates from multiple lenders.

Banks, credit unions, and online lenders each structure loans differently, so reviewing a variety of options gives you a clearer picture of what’s available.

Look beyond the APR*.

While the interest rate is important, it’s only part of the equation. Compare loan terms, fees, and whether the lender offers perks like no prepayment penalties.

Review your credit standing first.

Stronger credit typically means lower rates. Before you begin rate shopping, make sure your credit report is accurate and up to date. This will shape the offers you receive.

Evaluate the loan term carefully.

Longer terms usually mean lower monthly payments but higher total interest. Shorter terms may raise your payment, but they often cost less over time.

Check lender reputation and customer experience.

Reliable service, clear communication, and easy processing matter, especially during the payoff transition from your old loan to the new one.

If you're learning how to refinance an auto loan for the first time, comparing multiple offers is one of the most effective ways to uncover the best rate and ensure the refinance supports your broader financial goals.

Get more tips on finding the best auto loan refinance deal >

Conclusion: Should I Refinance My Auto Loan?

When timed well, auto loan refinancing is a powerful tool that can:

- Lower your monthly car payment

- Reduce the amount of interest you pay over time

- Help you pay off your car faster

If you’re ready to explore auto loan refinancing, click below to learn more about our auto loans. Or, if you want to keep exploring the benefits, check out our related content below.