How to Lower Your Car Payment… And More Benefits of Auto Loan Refinance

See all the ways refinancing your auto loan can help you.

Published Monday, May 4, 2026 to Advice

Most people searching for how to lower your car payment assume there’s only one solution: get a lower interest rate. But auto loan refinancing can do far more than trim your monthly bill.

In the right situation, it can help you remove a co signer, reduce your overall debt burden, and free up cash flow that makes everyday finances feel less tight. All without changing vehicles.

But first, learn more about the basics of auto loan refinancing >

These lesser known advantages are often overlooked, yet they’re exactly why refinancing can be a smart financial reset, not just a rate play.

Start With the Basics: What Does It Mean to Lower Your Car Payment?

Lowering your payment usually comes down to three levers:

- Reducing your interest rate

- Extending your loan term

- Restructuring the loan

Refinancing gives you the ability to use any combination of these moves, which makes it the most flexible solution.

Lower Your Monthly Payment by Reducing Your Rate

A lower rate reduces the amount of interest charged each month, which immediately lowers your payment. This works best if your credit has improved or if market rates have dropped since you took out the original loan. Even a small reduction can create noticeable savings over the life of the loan.

Lower Your Monthly Payment by Extending Your Loan Term

Refinancing can also lengthen the repayment timeline. Spreading the balance over more months creates a smaller monthly bill, which could be the fastest way to get immediate relief.

The trade-off is that you may pay more interest in total and take longer to repay your loan. But the short-term cash flow benefit is substantial for many borrowers.

Lower Your Monthly Payment by Restructuring Your Loan

This process is sort of a catch-all for the rest of the ways you can lower your car payment. Restructuring your loan may include:

- Removing a co-signer from the loan

- Negotiating lower fees or restrictive terms

- Removing unwanted add-ons like warranties, GAP or service contracts

These are just a few of the ways you can restructure your loan to lower your payments or get other benefits.

The Hidden Benefits of Auto Loan Refinance

Increase Your Monthly Cash Flow Without Changing Cars

A lower car payment puts money back into your budget immediately. That extra room can go toward savings, debt payoff, or daily expenses.

For households with tight month-to-month margins, even an extra $50–$150 can make unexpected costs much easier to manage.

Reduce Your Overall Debt Load

Refinancing can also decrease how much you pay in total interest. This usually happens when borrowers qualify for a lower rate after improving their credit or stabilizing their finances.

A cheaper interest rate reduces the lifetime cost of the loan, even if the payment amount stays similar.

Explore: How Auto Loan Refinancing Supports a Smart Debt Reduction Strategy >

Remove a Co Signer and Simplify Ownership

Many people refinance simply to remove a co signer. This is common after credit scores improve, relationships change, or borrowers want full financial independence.

Moving the loan into a single name can also make responsibilities clearer for both parties and help each person protect their credit history.

Improve Your Credit Profile

Refinancing creates an opportunity to build better credit over time. A new loan with a lower payment makes it easier to stay on track with consistent on time payments.

While the hard inquiry may cause a small temporary dip, the long-term impact of steady payment history often outweighs it.

When Refinancing Makes the Most Sense

Refinancing may be especially helpful when:

- Your credit score has gone up

- Interest rates are lower

- Your budget needs adjustment

It’s also the right move when your current loan has high fees or an uncompetitive rate. If you want to remove a co signer or reset your loan terms, refinancing is often the cleanest path.

Dive Deeper: Should I Refinance My Auto Loan? >

Quick Eligibility Checklist

Most lenders look for a few basic factors:

- Your credit score

- Remaining loan balance

- Age and mileage of the vehicle

Consistent payment history and proof of income also increase your chances of approval. These requirements vary, but most borrowers can check your eligibility in minutes.

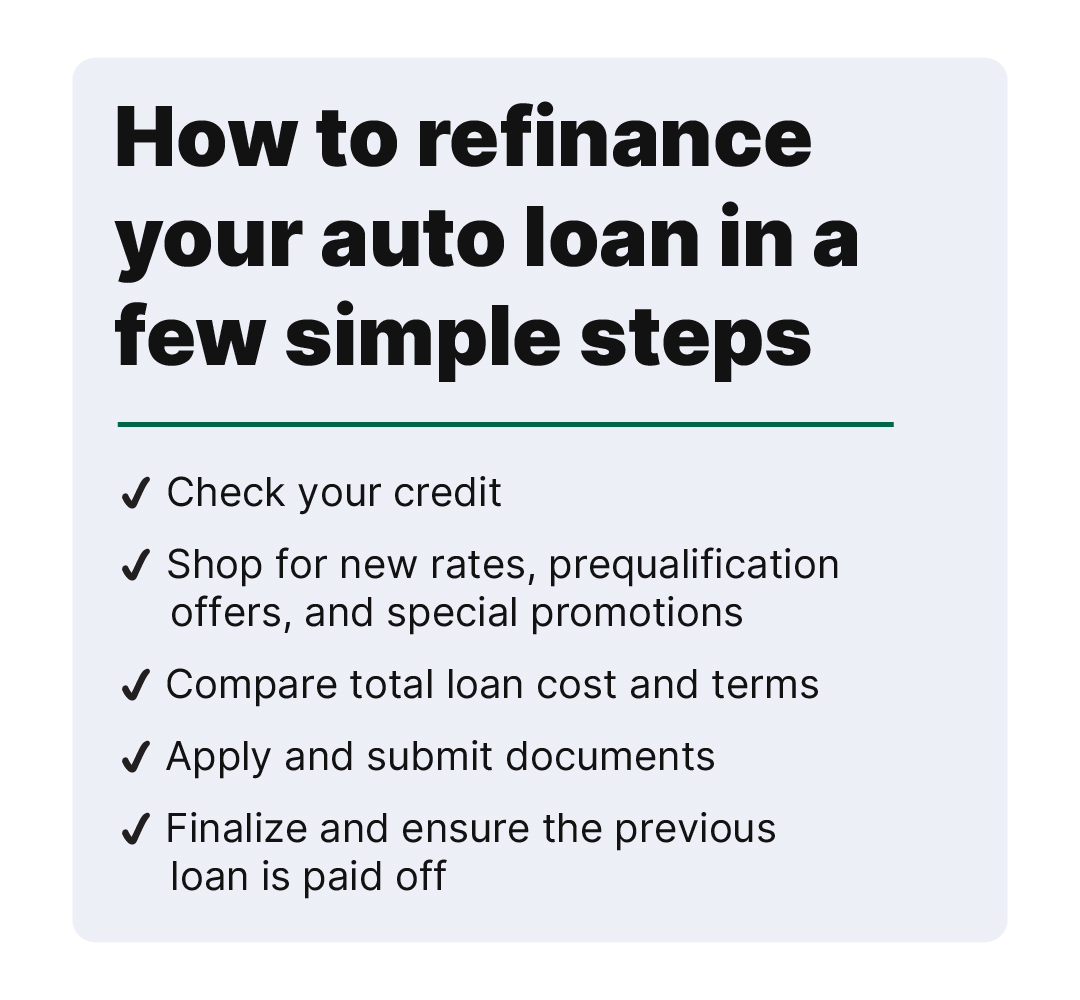

How to Refinance Your Auto Loan in a Few Simple Steps

Refinancing your auto loan is easy and takes just a few steps.

Start by reviewing your credit score and current loan details so you know what terms make sense. Then shop around for prequalification offers to compare potential rates and savings.

Once you find a loan that fits your goals, you’ll complete an application and submit documents like income verification and vehicle information. The new lender pays off your previous loan, and you begin making payments under the new terms.

Learn more about finding the best auto refinance rates >

Conclusion: Hidden Benefits of Auto Loan Refinance

Lowering your car payment is usually the main goal, but refinancing can deliver far more value than most people realize. It can help you improve cash flow, reduce debt, and take full ownership of your loan, all while keeping the same car. If you’re exploring ways to lower your payment, refinancing is one of the most effective tools available.

Learn more about our auto loan refinancing options, then see how much you could save with our auto refinance savings calculator. Or get more tips and information in the related content below.