Minimum Credit Score to Buy a Home: Tips to Get Your Credit in Homebuying Shape

Get the facts on credit requirements for buying a home.

Published Wednesday, April 1, 2026 to Advice

When you’re thinking about buying a home, one number tends to loom larger than the rest: your credit score. But what is the actual minimum score you need to make homeownership possible?

The answer isn’t so simple. There’s not a single cutoff number. Lenders look at credit differently depending on the loan program, your broader financial profile, and even how your score is calculated, meaning you may be closer to qualifying than you think.

Understanding the real minimum credit score requirements, and how lenders use them, can help you plan smarter, act sooner, and avoid costly assumptions as you prepare to buy a home.

Start at the Beginning: First-Time Homebuyer’s Guide >

Is There a Single Minimum Credit Score to Buy a Home?

The short answer is, no, there is no universal minimum credit score.

Minimum credit score requirements vary by loan program (such as conventional, FHA, VA, or USDA loans) and by individual lender. Some lenders may have higher standards and others may serve a wider range of credit scores and situations.

To sum it up, think of your credit score as the gatekeeper, but it doesn’t have the final say in whether or not you get approved.

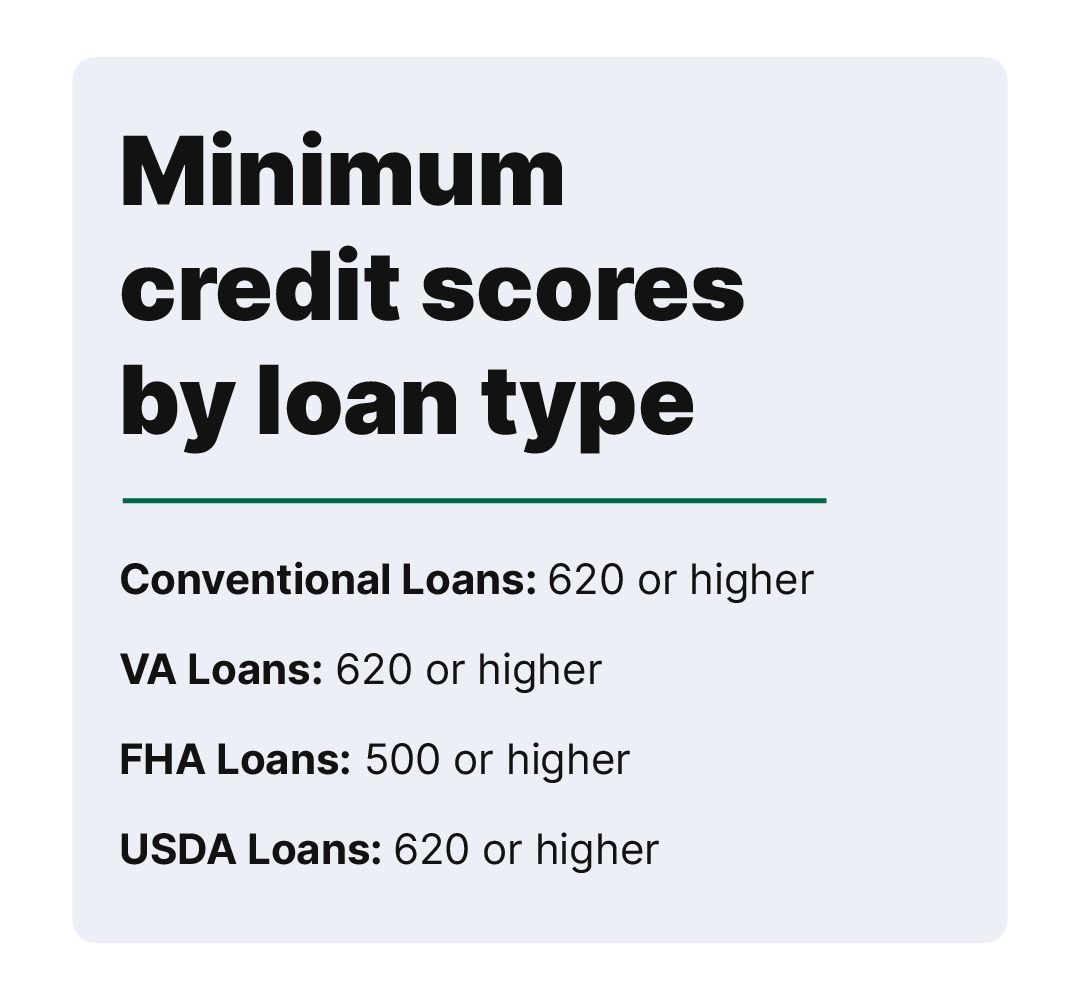

Minimum Credit Scores by Loan Type

While there isn’t a single minimum credit score for being approved for a mortgage, there are baselines you can shoot for, depending on the type you’re applying for.

Conventional Loans

Conventional mortgages are the most common type of mortgage and are not backed by the federal government. They generally require a credit score of 620 or higher to qualify. Better rates and terms are generally available to those with higher credit scores.

Credit Score to Shoot For: 620 or higher

VA Loans

VA loans are available through the Department of Veterans Affairs for servicemembers, veterans and their families to buy homes. There isn’t an official minimum credit score for VA loans, but the private lenders who issue them set their own standards. In 2026, 620 is the most common lender minimum.

Credit Score to Shoot For: 620 or higher

FHA Loans

A Federal Housing Administration (FHA) loan is a government-insured mortgage with more lenient qualification requirements. Credit scores of 580 and up may qualify with a 3.5% down payment, while scores between 500-579 may qualify with a 10% down payment.

However, some lenders may impose stricter requirements for approval. Availability of these loans is also more limited than other types, and they are not offered by all lenders.

Baseline Credit Score: 500 or higher

USDA Loans

USDA loans are zero-down-payment mortgages for eligible buyers, usually in rural areas. A score of 620 is usually required for general approval, but applicants can receive automatic approval with scores of 640 and higher.

Credit Score to Shoot For: 620 or higher

What Lenders Really Look at Alongside Your Credit Score

Your debt-to-income (DTI) ratio is one of the most important factors. Your DTI is the percentage of your gross monthly income (before taxes) that you spend on recurring debt. This is used by lenders to determine how much you can afford for your monthly mortgage payment.

Your payment history and credit behavior show the lender how reliable you are with paying back debt. And your employment and income stability tell them whether you’ll be able to pay your mortgage every month.

Finally, lenders will want to see bank statements and financial documents to see your cash reserves. A sizeable down payment will also help your chances of getting approved with a good rate.

What If Your Credit Score Is Below the Minimum?

If your credit score or any other credit factors miss the mark, it isn’t game over. You can improve your credit to work towards approval later.

Start by looking at your credit report and finding out where the issues are. Look at the following:

- Length of credit history. Closing credit accounts will have a negative impact on your score.

- Credit mix. You want a healthy mix of revolving and installment credit.

- Payment history. Make sure you’re paying the minimum amount on all your accounts on time.

When reviewing your credit, you may even find an error that, when corrected, qualifies you for mortgage approval.

Work with your lender to identify ways to improve your credit as you work towards homeownership.

Check out this video for some easy tips to improve your credit.

How Far in Advance Should You Check Your Credit?

Start checking your credit 6 – 12 months before you plan to buy. And, during this time, don’t open any new credit accounts, as new accounts have a negative impact on your credit score.

Checking your credit early can help you:

- Identify errors and have them corrected with the credit bureaus.

- Create a strategy to pay off debt and increase your available credit.

- Monitor your credit score as you make changes.

You’re entitled to one free credit report each year from all three credit bureaus without impacting your credit score. Plus, you can check your credit score free anytime with Credit Central, powered by SavvyMoney in Veridian digital banking and the mobile app.

The Bottom Line: Focus On Your Full Credit Report

So, what is the minimum credit score to buy a home?

To sum it all up, your credit score is only a part of what goes into qualifying for a mortgage. There is no universal minimum score, no matter the mortgage program you apply for.

What really matters is the broader picture of your credit report and overall financial situation.

And even if your credit’s not where it needs to be now, you can get there with a little help and a plan.

If you’re ready to explore your options, check out our mortgage products or schedule an appointment with a Mortgage Loan Advisor. Or explore more topics about homebuying below.