Saving for a Down Payment on a House: Are CDs The Way to Go?

Learn how a CD can protect your down payment savings and grow it faster.

Published Wednesday, April 1, 2026 to Advice

Saving for a down payment on a house can feel like walking a tightrope: you want your money to grow, but you can’t afford to lose it. This paradox may leave you wondering where you should keep your down payment money.

If you’re nearing your purchase timeframe, an investment might be too risky. But a standard savings account may not feel like enough.

Certificates of deposit (CDs), on the other hand, offer a middle ground that often gets overlooked. With predictable returns, federally insured protection, and timelines you can match to your home-buying plans, CDs can be a strategic tool for saving toward a down payment.

Where You Save Your Down Payment Matters

A down payment on a house is typically one of the largest cash savings goals you will have in your life. Unlike retirement, you have a fixed—or at least semi-fixed—timeline.

If your timeline is far off, you need to focus on growth. If your timeline is nearing, or at least narrowing, you need to focus on protecting your savings.

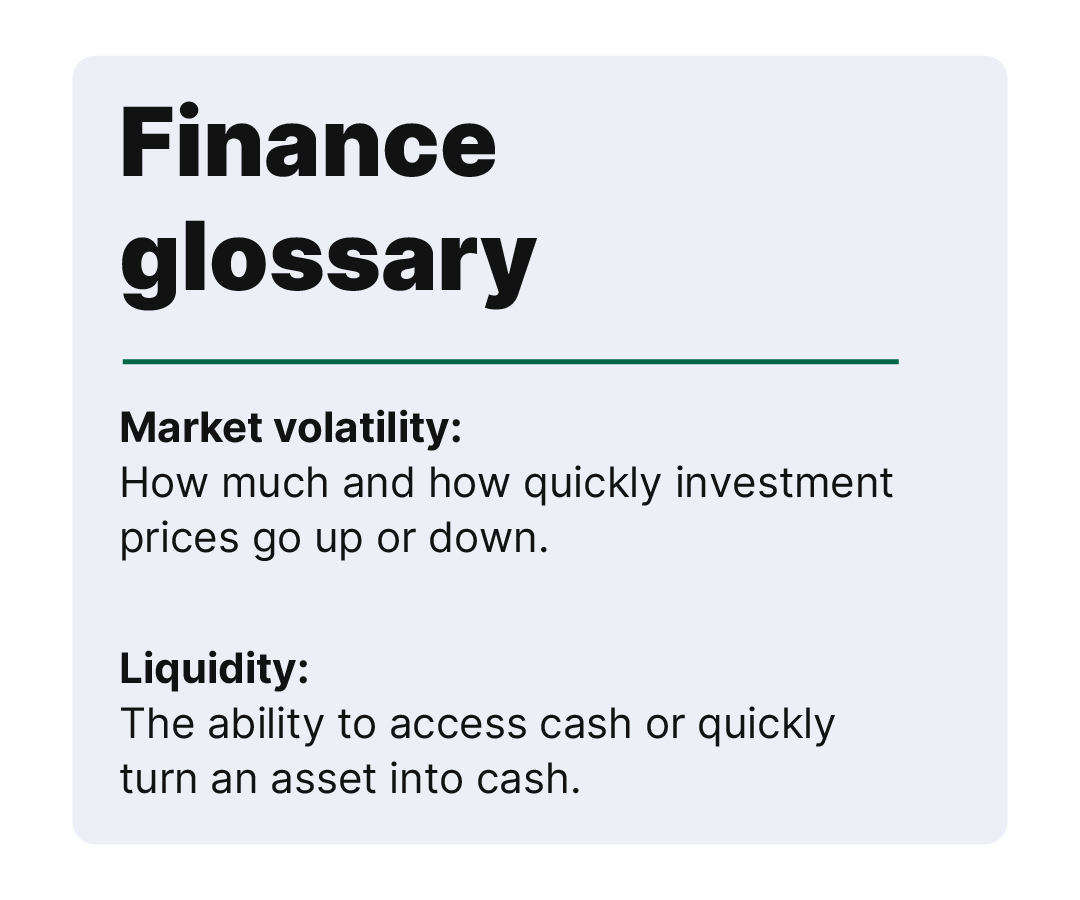

In all situations, you need to consider the balance between market volatility and liquidity needs.

- Market volatility: investments can earn a lot in a short amount of time, but a volatile or unpredictable market can cause your savings to lose value.

- Liquidity: this means having access to your funds. You’ll want to ensure your funds are available by your goal date.

What Is a CD and Why It Appeals to Homebuyers

A certificate of deposit, more commonly known as a CD, allows you to earn a fixed rate when you save your money for a set amount of time. That means your rate will not change for the duration of your CD’s term unless you withdraw your funds early.

Plus, CDs are federally insured by NCUA or FDIC, which makes them one of the safest most predictable investments you can get.

CDs may not be the magic tool to all your savings needs as you build towards your down payment goal. But they can be a useful part of your overall savings strategy or help you get one last boost as you near your target date.

Check It Out: See Our CD Rates, Terms and Specials >

When CDs Make Sense for Down Payment Savings

CDs will work best for you if you have a clear purchase timeline and want to protect what you’ve already saved. If you expect to buy within the next six months to three years, CDs can earn more interest than a typical savings account without exposing your down payment to market volatility.

CDs are especially appealing once your down payment savings balance becomes significant. Higher balances earning higher rates equal higher returns.

When the goal shifts from aggressive growth to protecting your savings, a CD with a fixed rate can provide peace of mind.

But CDs aren’t ideal for every buyer. If you’re trying to buy right now, or if you don’t have a defined timeline, the reduced flexibility may outweigh the benefits. Used intentionally, however, CDs can be a practical fit for buyers who value predictability and want a clear path from saving to closing.

How to Use CDs Strategically When Saving for a House

Simply put, you want to choose a CD with a term that ends just before you want to buy a home. And, even more importantly, you want to avoid terms that force you to withdraw funds early to buy.

Now that we’ve discussed the simple side of CD savings, let’s dive a little deeper with some strategies.

Consider Laddering for Flexibility

Laddering allows you to spread your savings across multiple CDs with different maturity dates. For example:

- One CD maturing in 6 months

- One in 12 months

- One in 18 months

This lets you balance growth with flexibility and access to your funds.

Learn More: Step Up Your Savings with a CD Ladder >

Keep Some Cash Liquid

Make sure to keep a portion of your down payment savings in a savings account that you have instant access to, preferably a high-interest savings account. This allows you to have flexibility for things like inspections, earnest money, or if your plans have to change.

Potential Downsides to Consider Before You Open a CD

Like we said earlier, CDs aren’t a magic solution. There are a few drawbacks.

- Early withdrawal penalties and fees.

- Reduced flexibility compared to savings accounts.

- Your rate is locked in for the full term, even if rates go up after you open your CD.

That said, if you plan it right and use them intentionally, CDs are a great tool for helping grow your down payment savings. Any drawbacks are easy to navigate around.

A Thoughtful Approach to Down Payment Savings

When saving for a down payment on a house, the goal isn’t maximum return... it’s certainty. CDs can offer a dependable way to protect your savings and earn predictable interest as you work toward buying a home.

If stability matters to you, take a closer look at our CD options to see how they might fit your plan.

And when you’re ready for the next step, our first-time homebuyer guide can help you navigate the full process.