How to Get Pre-Approved for a Mortgage

Learn why this important step is the starting line for your homebuying experience.

Published Wednesday, April 1, 2026 to Advice

Before you tour open houses, fall in love with a kitchen, or imagine where the couch will go, there’s one step that can make or break your first homebuying experience: mortgage pre-approval.

If you’re wondering how to get pre-approved for a mortgage, you’re asking the right question. Pre-approval isn’t just paperwork. It’s how you find out what kind of home you can afford, how competitive your offers will be, and whether sellers will take you seriously.

For first time buyers especially, skipping this step can lead to wasted time, missed opportunities, or unpleasant surprises later in the process. It could even make it harder to find a realtor to work with.

Below, we’ll break down exactly how to get pre-approved for a mortgage, what lenders look for, and how this step fits into the bigger picture of buying your first home.

Start at the Beginning: How to Buy Your First Home >

What is Mortgage Pre-Approval?

Before you dive into how to get pre-approved for a mortgage, you should understand what it means.

Pre-approval is a financial institution’s tentative commitment to lend money to you, up to a certain amount, to purchase a home. The final decision will depend on a few conditions, like the sale price being at or below the appraised amount.

A pre-approval letter signals to your realtor, any sellers and their real estate agents, that you are a serious buyer and are unlikely to encounter any major hiccups in the mortgage process.

Why Mortgage Pre-Approval Matters for First-Time Buyers

For first-time homebuyers (and all homebuyers, for that matter), pre-approval can help in so many ways. Here are a few points we’ll focus on:

- It helps you set a realistic budget. You, and anyone involved in the sale, know your maximum purchase price. That way, you won’t get carried away when you see a house a little out of your price range.

- Pre-approval strengthens your offers. Mortgage approval is one fewer thing a potential seller must worry about when receiving an offer from you.

- Realtors want to work with you. In fact, many realtors won’t even tour homes with you until you have a pre-approval letter from a financial institution.

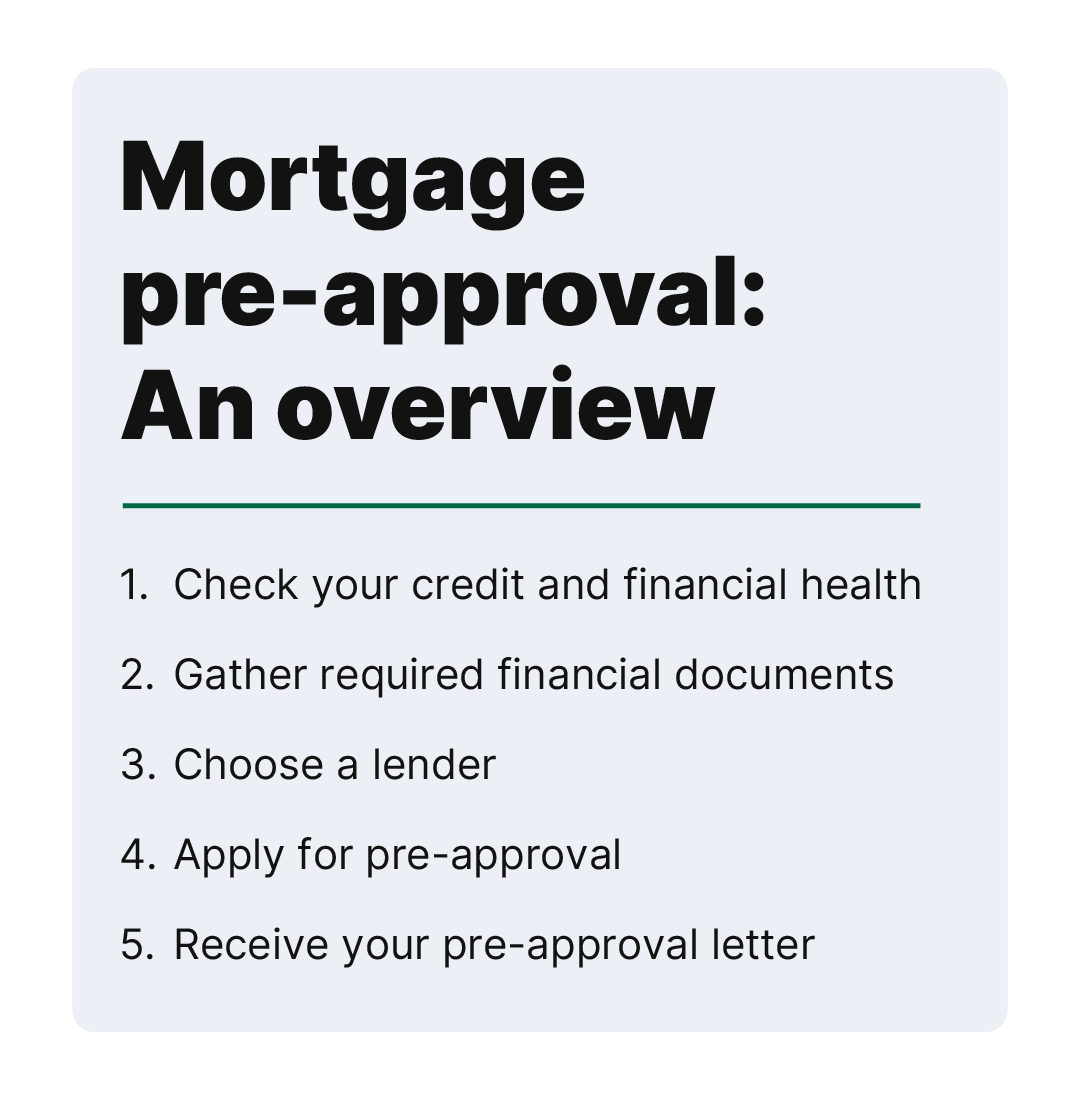

How to Get Pre-Approved for a Mortgage: Step by Step

Now that we’ve gone over why pre-approval is such an important step in the homebuying experience, here’s what you can expect from the process:

Step 1: Check Your Credit and Financial Health

Check your credit score and debt-to-income ratio. Many conventional loans require a credit score of 620 or higher, and a debt-to-income ratio of 43% or less.

Check out Credit Central, powered by Savvy Money in Veridian digital banking to get started.

The figures noted above are just industry baselines, and actual requirements will depend on your mortgage type, your financial institution and your personal financial situation.

Learn More: Get Your Credit in Homebuying Shape >

If you find a problem with your credit score early, your lender can help you look for solutions before you officially apply for pre-approval.

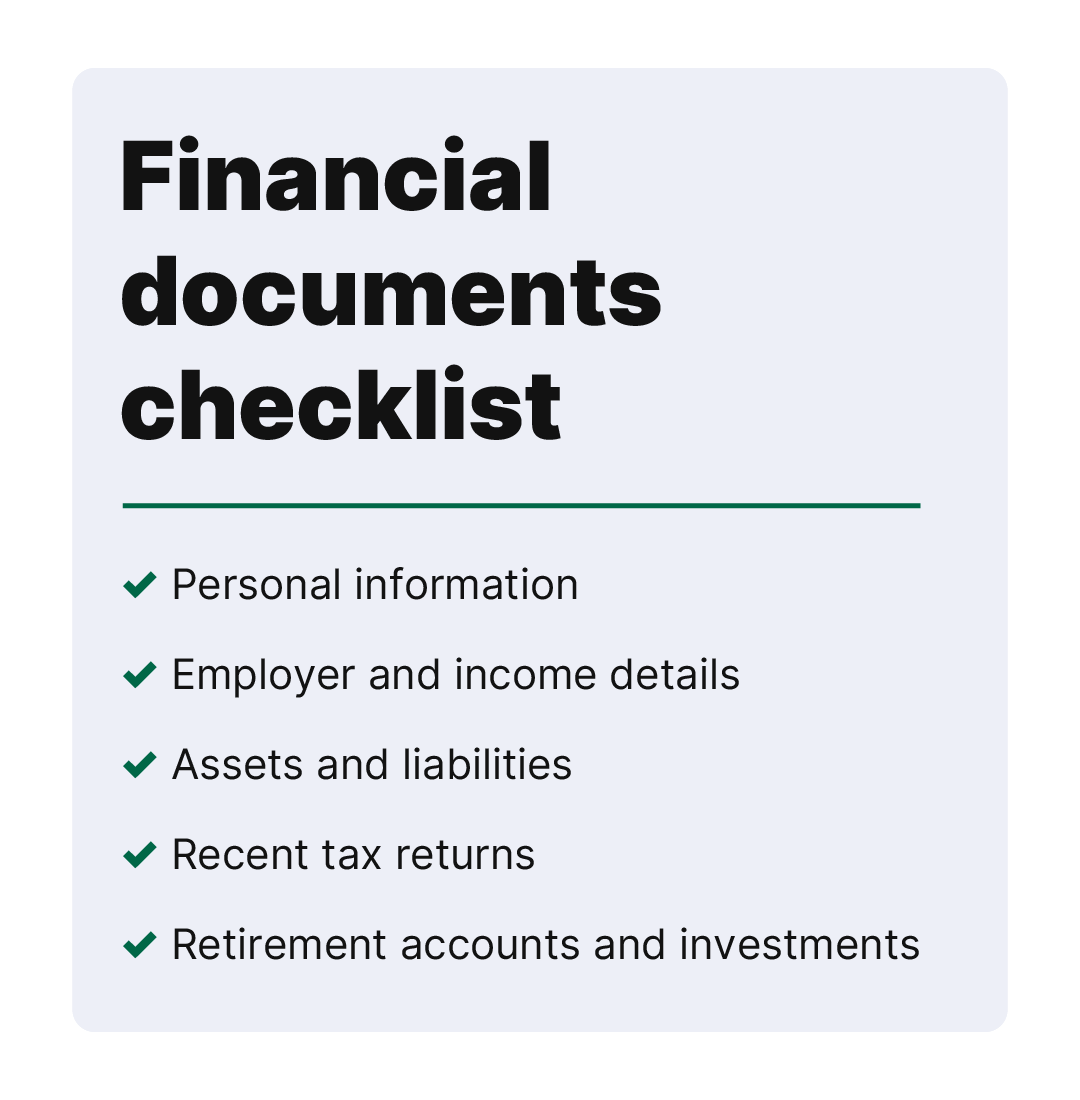

Step 2: Gather Required Financial Documents

Now it’s time to get all your documents together. Here’s a quick checklist of what you may need:

Get these files together and keep them in a physical folder to bring with you to your mortgage appointment. Or you can store digital versions of everything in a cloud folder, in Google Drive, for example.

- Your personal information and identification.

- Employment and income details.

- A list of your assets and liabilities, like bank statements, or other long-term debts, such as auto loans or student loans.

- Details about the home you are buying.

- Recent tax returns.

- Retirement and investment accounts.

Step 3: Choose a Lender (or Multiple Lenders)

Now, it’s time to shop around and find the best rates and terms. Remember, you can get pre-approved at more than one financial institution.

For obvious reasons, we’re partial to credit unions, but be sure to look at banks and mortgage brokers as well. You can even get pre-approval for one of each to compare rates, terms and conditions.

Step 4: Submit a Mortgage Pre-Approval Application

It’s finally time to submit your application for pre-approval! Check your preferred financial institution’s website to see if you can start your application there.

Once you get started, expect communication from your lender to guide you through the process and help you pick the best mortgage type for pre-approval.

At this time, they’ll run a hard credit inquiry to make sure you don’t have any issues that would prevent mortgage approval, and to verify how much you can spend on a house.

Step 5: Receive Your Pre-Approval Letter

If everything looks good, you can expect your pre-approval letter in as little as one day after you submit your application. It will include your maximum purchase price, your mortgage type, and any conditions that need to be met before final approval.

Share your pre-approval letter with your realtor. This tends to be the final green light to start touring houses.

In most cases, your pre-approval is valid for 90 days. If your home search lasts longer than that, you may need to re-apply for pre-approval.

Final Thoughts: Get Pre-Approved Before You Fall in Love with a House

Pre-approval is your most valuable tool when you start shopping for homes. It gives you, your realtor, and potential buyers peace of mind to know you’re a serious buyer.

Remember, you don’t need to use your full pre-approval amount. Be sure to account for things like maintenance, repairs, taxes and insurance before you purchase your home.

If you’re ready to start the pre-approval process, you can start with us online or on your mobile device. If you’re not sure, you can schedule an appointment with one of our experts, and we’ll talk you through the options.

Click below to check it out or explore more content for first-time homebuyers.