Understanding Your Credit Report and How to Monitor It

Learn what’s in your credit report and how monitoring it can help you improve your financial health.

Published Friday, January 2, 2026 to Advice

Your credit score is kind of like your financial fingerprint. It's completely unique to you, and incredibly valuable. Yet most people only look at their credit report once per year, if at all.

These days, monitoring your credit report has never been easier. If you're considering a financial refresh, be sure to include credit monitoring as part of your plan - it could save you money and stress.

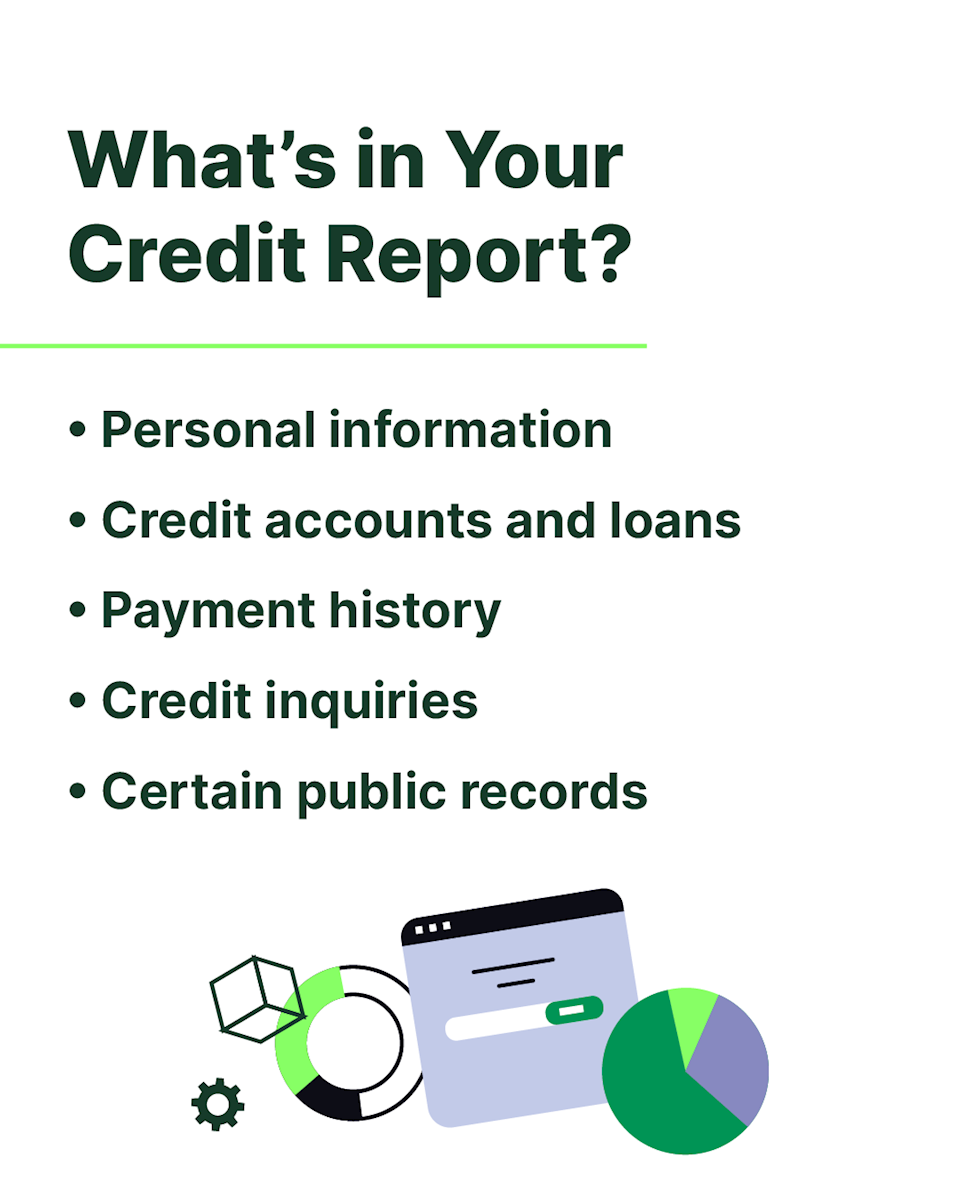

What Is a Credit Report and Why It Matters

Your credit report is a snapshot of your credit history. It contains these key elements:

- Your personal information.

- Credit accounts and loans.

- Payment history for each account.

- Credit inquiries.

- Certain public records.

It may seem obvious that lenders and credit card companies will check your credit score when you apply for loans. But did you know that even landlords check your credit report to get an understanding of how well you manage your finances before renting to you?

In some cases, even prospective employers may look at your credit report.

A strong, accurate report can help you qualify for lower interest rates, better loan terms, and improved access to credit. On the other hand, errors or missed updates could cost you money or opportunities.

Common Misconceptions About Credit Reports

“I only need to check my credit if I’m applying for a loan.”

Monitoring your credit report regularly can help you catch errors and give you a chance to correct them early. That way, when you do apply for a loan or credit card, there are no issues with getting approved.

“Credit report errors are rare.”

A report by Consumer Reports and WorkMoney discovered that 44% of those who checked their credit report found at least one error.

“Checking my own credit report can lower my credit score.”

Checking your own credit report counts as a soft inquiry, which doesn’t impact your credit score. And you are entitled to one free credit report annually from each of the three credit bureaus: Experian, Equifax and TransUnion.

Only hard inquiries – from lenders checking your credit during an application – can cause small, temporary dips.

How to Access Your Credit Report

There are a few different ways to monitor your credit report.

Annual Credit Report

As stated above, you are entitled to one free credit report each year from all three credit bureaus in the United States. Go to annualcreditreport.com to get started.

You may get all three of them at once or spread them out through the year to give yourself a chance to spot errors that may arise between credit checks.

Online Banking Credit Tools

Some online banking apps through your financial institution, credit card provider and more, may include free credit monitoring.

At Veridian, for example, our members have access to Credit Central powered by Savvy Money when they log into online banking or our mobile app. You can check your credit score anytime, see a breakdown of key factors, and get personalized insights to help improve your credit health – all without affecting your score.

Key Metrics to Watch on Your Credit Report

When reviewing your report, focus on a few core areas:

- Payment History: Late or missed payments can have the biggest impact on your score.

- Credit Utilization: Aim to use less than 30% of your available credit.

- Length of Credit History: Older accounts show stability, so keep long-term accounts open.

- Inquiries and New Accounts: Too many recent applications can lower your score temporarily.

Your credit score is not included in your credit report, but you should keep an eye on that as well. You can use online banking tools like Credit Central to monitor your score.

By keeping an eye on these elements, you’ll understand what influences your credit—and what to adjust to strengthen it.

Steps to Monitor and Protect Your Credit

Monitoring your credit regularly helps you act fast if something changes unexpectedly. Try these habits:

- Set up alerts and notifications through your credit monitoring tool.

- Review reports quarterly to check for errors or signs of fraud. Use online banking tools when necessary if you’ve already claimed your free annual credit reports.

- Report inaccuracies quickly to the credit bureaus.

- Pay on time and pay down balances to maintain a strong score.

- Limit new credit applications to avoid unnecessary inquiries.

Using Credit Central to Stay Ahead

Credit Central takes the guesswork out of monitoring your credit. You’ll see your credit score, understand the factors behind it, and get instant updates if something changes.

Plus, you can explore personalized recommendations to help you build or maintain strong credit – all right from your Veridian online banking or mobile app.

When you stay informed, you stay empowered. Credit Central helps you make confident, proactive decisions that support your overall financial well-being.

Final Thoughts: How to Monitor Your Credit

Your credit report is more than a reflection of your past. It’s a tool for shaping your financial future. Monitoring it regularly can help you save money, catch fraud early, and make smarter borrowing decisions.

Take a few minutes today to check your credit report or explore Credit Central in Veridian’s online banking or mobile app to see how simple credit monitoring can be. Or, if you’re not a Veridian member, check your financial institution or credit card provider’s app to see if they offer this.