How Does a HELOC Work?

A HELOC could be the cornerstone of your debt detox.

Published Thursday, February 5, 2026 to Advice

Many homeowners know they have equity in their homes, but few realize how powerful it can be as a financial tool. It can be an effective way to simplify your debt, lower your payments or pay off your debt faster.

If you’re looking for a flexible way to jumpstart your debt detox, a HELOC – or Home Equity Line of Credit – might be the answer.

Understanding how a HELOC works can help you tap into your home’s value strategically, giving you the flexibility to support a smarter, more intentional debt detox.

What is a HELOC?

A home equity loan allows you to use your equity – the difference between your home’s value and your mortgage balance – for financing. You can use it to refinance other debt, home renovations, education and more.

A HELOC is a type of home equity loan with one major difference. A HELOC is an open line of credit you can borrow from repeatedly as needed, as long as you don’t exceed your limit.

You can use a HELOC to help consolidate higher-interest debt to help you lower your monthly payments or pay off your debt sooner. You can refinance a single loan or credit card, or you can merge multiple loans together in a HELOC.

Learn More: How a HELOC Can Help You Achieve Financial Freedom

How Does a HELOC Work?

As stated above, a HELOC lets you borrow against your home’s equity as needed.

Your credit limit will be the amount of equity you have in your home when you apply. Your credit limit won’t increase automatically as your equity increases.

Interest rates may vary depending on your financial institution, and many come with a fixed rate for a certain amount of time. After the original time period, the rates become variable.

At Veridian, for example, our HELOCs are 20-year loans that have a fixed rate for the first five or 10 years. After those five or 10 years are up, your rate becomes variable and may change depending on market conditions.

The monthly payment on a HELOC is usually a pre-set percentage of your balance, but you are free to pay more as you see fit.

If you have a HELOC at Veridian, for example, the minimum payment would be 1% of your balance each month. So, if you have a $10,000 balance, you must pay at least $100 each month.

As you can see, a HELOC is a flexible way to manage your debt.

HELOC vs. Other Debt

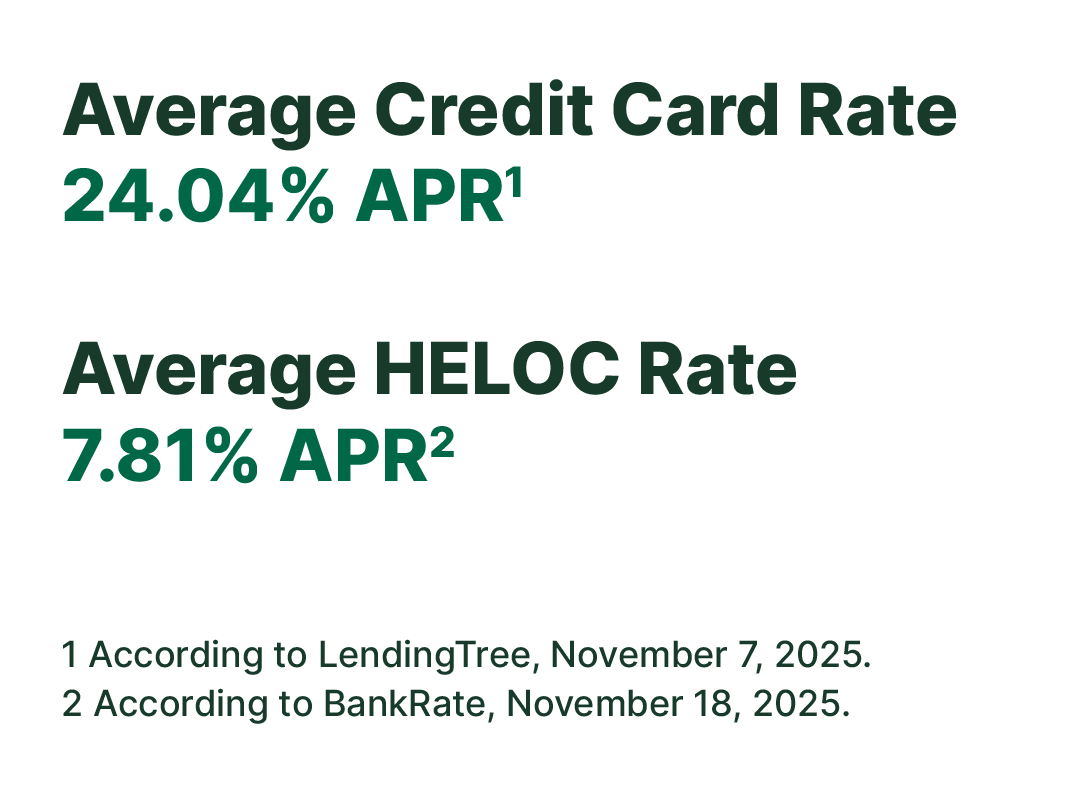

The main difference between a HELOC and other debt is the rate. HELOC rates tend to be lower than other types of consumer debt like personal loans and credit cards.

The other main difference is that you must be a home owner to get a HELOC. If you don’t own a home, you may look at low-interest credit cards, personal loans or auto loan refinancing to help you in your debt detox.

How a HELOC Can Support Your Debt Detox Journey

There are a couple of different ways a HELOC can support your debt detox.

First, it can help free up cash flow. If your monthly payments are high, a HELOC can lower payments to free up some cash for your household budget.

Or, if your goal is to pay off debt, a HELOC can help with that. With a lower interest rate, you’ll pay off debt faster because less interest will accrue each month.

The Cornerstone of Your Debt Detox

A HELOC is one of the most flexible loans out there. It has lower rates than most other consumer loans and offers easy payment options – perfect for your debt detox.

If you’re a homeowner and want to learn more about our home equity loans, click below. Or you can learn more about starting your debt detox your way.