Debt Detox Made Simple: Consolidation and Smart Loan Options

See the tools you can use to take control of your loans.

Published Thursday, February 5, 2026 to Advice

If your monthly payments feel like they’re pulling you in every direction, you’re not alone.

The good news? With the right tools — like debt consolidation, auto refinancing, and personal loans — you can take back control, simplify your payments, and start moving toward financial confidence again.

In this debt detox guide, we’ll talk about how the different options can help you save money or pay down your debt faster.

For example, debt consolidation can simplify your debt and save you money each month with a lower interest rate. Refinancing existing debt, like an auto loan or mortgage, can lower your monthly payments or help you pay off your loans sooner.

You don’t need to tackle everything at once. The key is understanding which tools fit your goals and how each one can help you clean up your financial picture, step by step. In this guide, we’ll explore different strategies, how they work, and how to choose the right approach for your own debt detox.

What is Debt Consolidation?

Think about your current debt. How many different bills are you paying each month?

Depending on your current situation, you may have:

- Student loan payments

- Credit card bills

- Personal loans

- Auto loans

- Medical bills

And some people have many more than what’s listed above with varying interest rates. With debt consolidation, you can combine multiple loans into one monthly payment with one interest rate.

There are a few clear advantages to using debt consolidation.

Simplify Your Bills

Instead of trying to remember to pay multiple bills, or forgetting about bills you have on autopay, you can simplify your debt into one monthly payment. Your student loans, high-interest credit card bill and that auto loan could all be taken care of with one monthly payment.

Lower Interest Rates

When you consolidate debt, you should also try to get a lower interest rate than what your current loans carry. This gives you the option to either pay less each month or pay off your loans sooner while paying the same amount.

Now, let’s talk about one of the best ways to consolidate debt to save money.

Using Home Equity to Consolidate Debt

If you’re a homeowner, a home equity loan or HELOC is a great option for consolidating debt.

With a home equity loan, you can borrow against the equity you have in your home. To determine your equity, you subtract the amount you currently owe on your mortgage from the value of your home.

So, if your home’s value is $350,000 and your current mortgage balance is $250,000, you have $100,000 in equity. That means you could borrow $100,000 with a home equity loan.

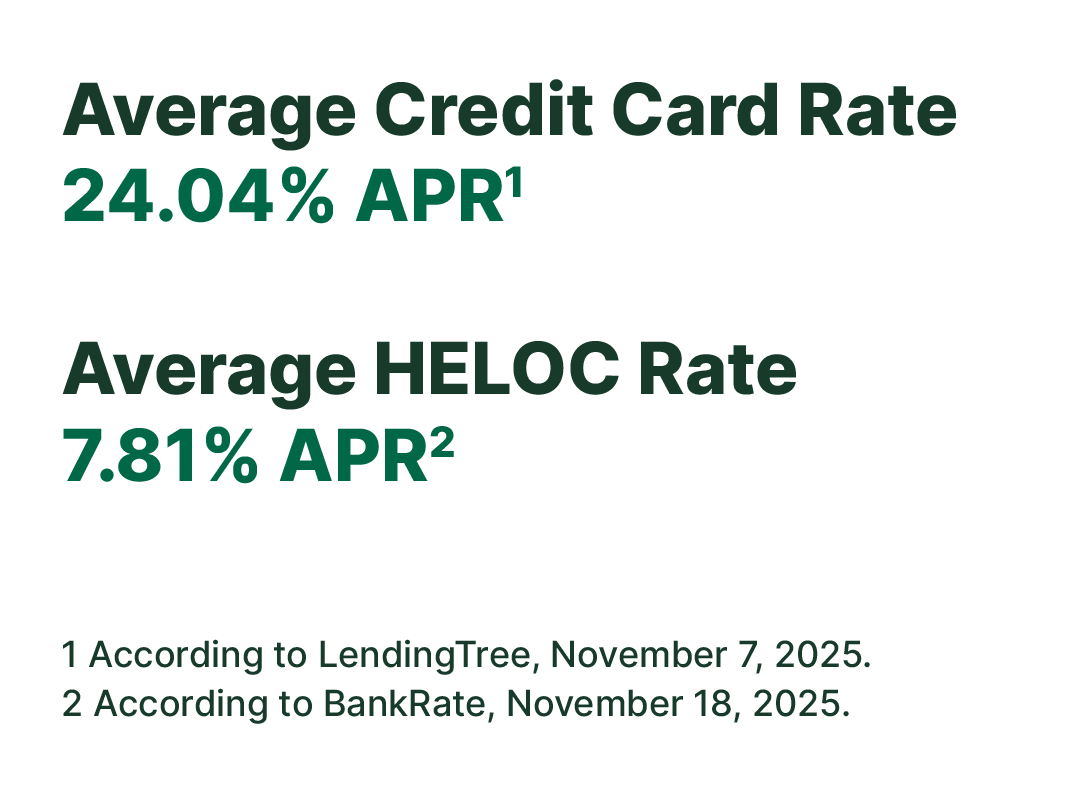

Home equity loans are great options for debt consolidation because they have lower rates than many other types of consumer debt like credit cards.

For example, the average credit card rate in November 2025 was 24.04% APR1. The average HELOC interest rate during the same time period was 7.81% APR2.

You may notice that we keep using the terms “home equity loan” and “HELOC.” They’re similar loans, but have a key difference.

A standard home equity loan allows you to borrow a one-time lump sum and then make fixed monthly payments. The maximum loan amount is equal to the equity you have in your home.

A HELOC, on the other hand, is an open line of credit that you can borrow from over and over again as needed. Your maximum balance is the amount of equity you have in your home as of when you apply for the loan.

Since you can borrow from your HELOC repeatedly, your minimum monthly payment may change from time to time. At Veridian, for example, the minimum monthly payment on a HELOC is 1% of your balance or $50, whichever is more.

Learn More: How a HELOC Can Help You Achieve Financial Freedom

Veridian Home Equity Loans and HELOCs offer competitive rates and flexible repayment terms that can help you consolidate debt wisely.

Learn more about using your home’s equity to consolidate loans.

Lower Your Credit Card Interest

Credit card interest can get expensive if you carry a balance from month to month. But there are a few ways you may be able to get a lower rate and save some money each month and in the long run.

Negotiate a Lower Rate

Sometimes, if you’ve been a responsible cardholder, your credit card issuer may be willing to offer you a lower rate if you call them and ask.

Transfer Your Balance

If you’ve improved your credit score since you opened your current credit card, you may qualify for a lower rate on a different credit card. In most cases, transferring a balance is easy and can be done online either while applying for the card, or after the new card is opened.

Many credit cards charge a small balance transfer fee. So, make sure any balance transfer fees don’t offset the savings from a lower rate.

Many credit cards offer rewards or cash back. While this is separate from a rate reduction, you could consider these bonuses to be part of your overall savings.

With a Visa Credit Card from Veridian, you can take advantage of competitive balance transfer rates to help pay down high-interest debt faster. Our credit card rates currently offer interest rates as low as [RateToken]% APR*.

Refinance Your Auto Loan to Free Up Cash

If you’re wondering how to save more on your auto loan each month, or are hoping to pay it off sooner, refinancing may be the answer.

When you refinance your auto loan, you close your existing car loan and move the remaining balance into a new one, usually with a new lender. The new loan should include a lower rate or a shorter repayment period, depending on your goals.

There are several potential benefits to refinancing your auto loan.

Save More Each Month

If you transfer your balance to an auto loan with a lower rate, you could reduce your monthly payment. This could free up cash flow for other needs in your life or to pay off other debts quicker.

Pay Off Your Loans Faster

If you’re okay with paying the same amount each month, you may be able to pay off your debt sooner with a lower interest rate.

Auto loan refinancing at Veridian can help you lower your rate and free up money to tackle other debt goals.

Learn more about auto refinancing.

Simplify Your Payments with a Personal Loan

Personal loans are another common strategy for consolidating debt, especially if you don’t own a home or don’t want to borrow against it.

With a personal loan, you can consolidate multiple loans, like credit cards, student loans and more into one fixed monthly payment. Personal loans don’t always have the lowest rates, but they are still lower than many other types of consumer debt.

When you get a personal loan, you borrow a lump sum and make fixed payments for the full term of the loan. Many times, personal loans are available for terms between 12 – 60 months, but this may vary depending on your financial institution.

Veridian Personal Loans make it easier to consolidate debt and stay on track with flexible terms and affordable rates.

See how a personal loan could simplify your debt.

Tips to Stay in Control After Your Debt Detox

Consolidating or refinancing your debt is a huge step toward getting things back on track. Now the goal is to keep that momentum going.

A few simple habits can make your debt detox stick and help you avoid slipping back into old stress patterns. Here are some easy ways to stay in control:

Build a Budget

Nothing complicated. Just a clear picture of what’s coming in, what’s going out, and where you have room to breathe. Even a basic budget can make your new consolidated payment feel more manageable.

Set Up Automatic Payments

Autopay is your best friend. It helps you stay consistent, avoid late fees, and keep your payoff plan moving in the right direction without extra effort.

Hit Pause on New Debt

Try to avoid taking on additional credit while you’re still paying down your existing balance. If surprises pop up, a small emergency fund can keep you from reaching for high-interest options again.

Check In with Your Finances Regularly

A quick monthly review, plus a deeper look once or twice a year can help you adjust your plan as your life or goals change.

Staying on track doesn’t require a major overhaul. Just a few steady habits can turn your debt consolidation strategy into long-term financial control.

Frequently Asked Questions

What are some ways for me to take control of my debt this year?

You can utilize options like debt reconsolidation, auto loan refinancing, and balance transfer credit cards to get started.

How do I consolidate my debt?

You can consolidate your debt using a home equity loan or HELOC, a personal loan or a balance transfer credit card. A HELOC could be your best option if you own a home and have equity built up.

What are the benefits of debt consolidation?

When you consolidate your debt, you simplify all your bills into one simple payment. Plus, you may be able to get a lower rate so you can either pay off your debt sooner or lower your monthly payments.

Ready to Take the Next Step?

A debt detox isn’t one-size-fits-all. Sometimes the answer is debt consolidation; sometimes it’s refinancing; and, sometimes, it’s both.

At Veridian, we can help you take the steps you need to get your debt under control so you can reach your goals and achieve your successful financial future.

If you’re ready to start your debt detox, explore the content below to get started.