You Deserve the Upgrade: Financial Planning Without Stress

Upgrade your life without sacrificing future flexibility.

Published Monday, June 1, 2026 to Advice

Wanting more isn’t reckless… It’s natural!

Life upgrades come in many forms:

- Home renovations

- New vehicles

- Weddings (yep, upgrading your family counts)

- Vacations

But the fact of the matter is so many people say “no” to life upgrades, and it’s not always because they can’t afford it. In many cases, it’s because they fear future regret.

Stress over making life upgrades stems from uncertainty, not the choice itself. Have you ever been on the fence about a purchase and asked yourself any of these questions:

What if I use up all my savings and have an emergency later?

Is this something I really need?

Is this an irresponsible decision?

Financial planning for life upgrades isn’t always about need. Sometimes making the upgrades you want can improve your whole life, helping you feel happier, healthier and more productive.

So where does the confidence to say “yes” to life upgrades come from? It comes from financial confidence… and financial confidence comes from financial planning.

With the right financial tools, life upgrades and experiences may be closer to reality than you realize.

Wanting Better Is a Strength, Not a Flaw in Financial Planning

When you want to make upgrades, it’s often a sign that your life is changing. And growth naturally comes with new needs and expectations.

For example, maybe you got a new job with a pay raise and the opportunity to work from home. Upgrading that spare room into a home office will give you the opportunity to be comfortable during the workday.

Or maybe you and the love of your life decided to tie the knot. You may want to upgrade your vehicle to something more comfortable for both of you and your growing family.

The point is, life upgrades aren’t always indulgences or lapses in discipline. Sometimes they are necessary to make sure your world fits where your life is right now.

The key is to understand your financial situation and use the right tools. If you can do that, you’ll have the financial confidence to enjoy life without the stress.

Why Financial Stress Follows Uncertainty, Not Spending

Financial stress over how to afford lifestyle upgrades usually shows up when you can’t clearly answer, “What happens next?” It’s rarely about the upgrade itself. It’s about the unknowns attached to it.

When a plan feels vague, your brain fills in worst case scenarios. When the plan is clear, the same decision feels lighter.

Stressor: a predictable payment that still feels restrictive

You might afford the payment comfortably, but it leaves little room to adjust.

The stress comes from feeling locked in, not from the payment amount.

People start wondering what they could change if their income shifts or a new expense appears. The solution is not removing the payment, but reshaping it so it creates flexibility instead of pressure.

This is where adjusting terms or lowering a monthly obligation can turn a fixed cost into a supportive one.

Stressor: a meaningful one time expense with no recovery plan

Big moments are often exciting and heavy at the same time. The worry shows up afterward, when it’s unclear how long the financial impact will last.

Stress drops when the expense has defined edges. A clear monthly amount and a clear payoff timeline turn the upgrade into a chapter instead of an open question.

That structure protects confidence and makes it easier to recover.

Stressor: convenience spending that lingers longer than expected

Sometimes an upgrade goes on a card because it’s fast and available. The stress comes later, when the balance sticks around with no clear payoff path.

Clarity comes from deciding what paid off looks like before the balance grows. With simple boundaries and visibility, credit supports confidence instead of adding background anxiety.

The improvement is not spending less. It’s knowing how the decision fits before saying yes.

Different Life Upgrades Require Different Financial Strategies

Imagine you’re in the kitchen, making a delicious apple pie and fresh vanilla ice cream from scratch. Do both of those items require the same cooking method?

Absolutely not! The pie needs to go into the oven and the ice cream needs to go in the freezer (or use liquid nitrogen, but this is hardly the place to learn about something like that).

Paying for upgrades is the same. Different upgrades require different financial strategies.

For example, you may not want to use the same funding strategy for a home renovation as you would for buying a few pieces of home office furniture or paying for a family vacation.

Projects with predictable and fixed costs may use fixed loans. For ongoing projects and projects with variable costs, you may need more flexible financing options.

In short, your money strategy should match the nature of the upgrade.

Flexibility Is a Planning Tool, Not a Safety Net

Having flexibility in your budget gives you more wiggle room when paying for your life upgrades. That’s why you may want to look for ways to free up room in your everyday spending when you’re preparing for a major expense.

And we don’t just mean “cut a streaming service” or “make coffee at home.” There may be ways for you to lower payments on other debts like your auto loan.

A Lending Tree survey revealed that refinancers saved an average of $142 per month when they refinanced their auto loan. Assuming you also save that much each month, that’s extra money you could put towards your upcoming project.

Does this mean you have a bad auto loan? No!

Refinancing your auto loan is about alignment with current life, not fixing past mistakes. Your financial tools and planning should adapt as your life evolves.

Intentional Spending Builds Confidence Over Time

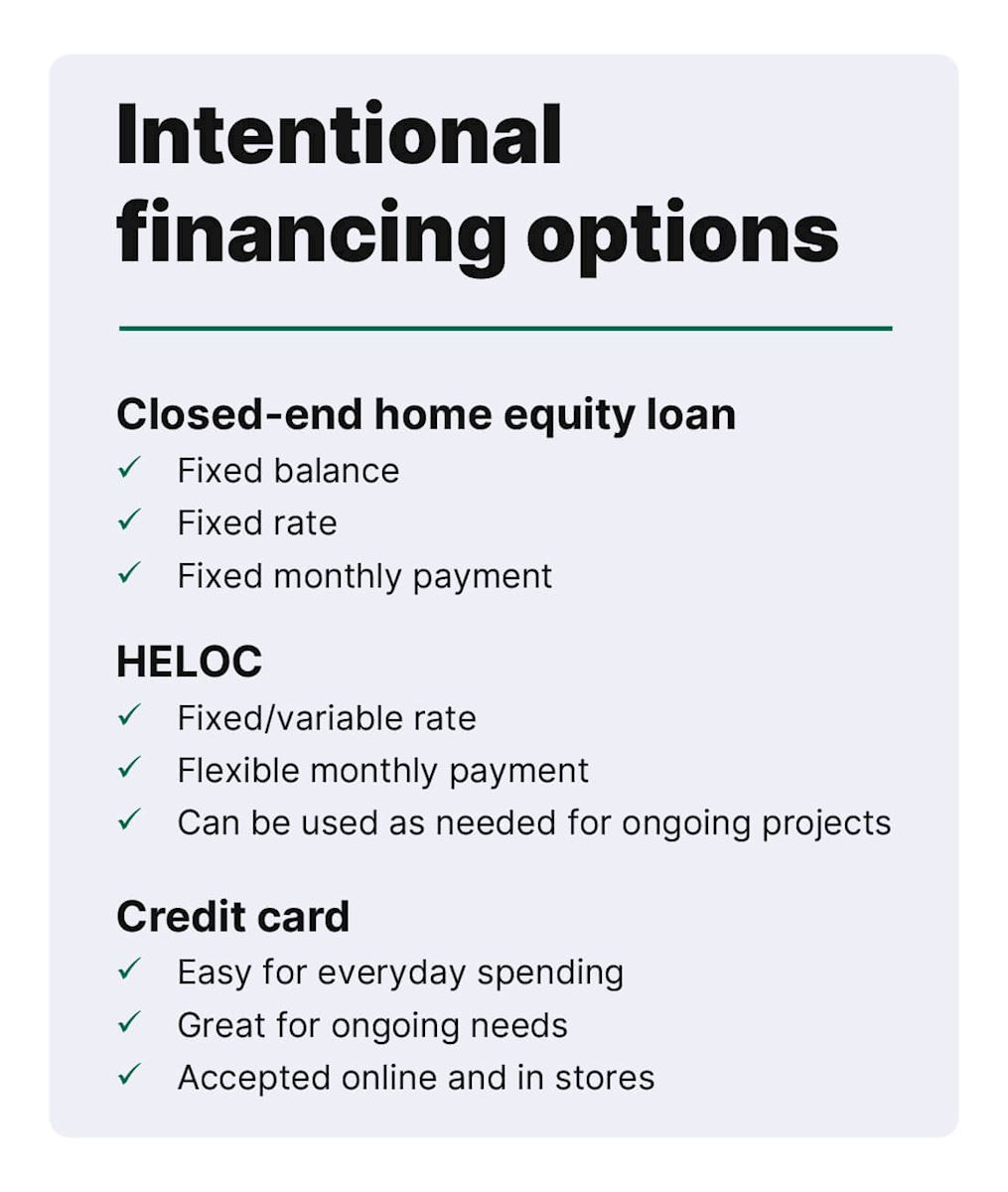

Fixed cost projects are easy to define. You can get a closed-ended loan (like a home equity loan) that has a defined balance, rate and monthly payment.

Where you need to be a little more disciplined is when your project has variable costs with an open line of credit, like a home equity line of credit (HELOC) or a credit card. With an open line of credit, you still need to ensure you’re spending intentionally.

A HELOC or a credit card shouldn't be treated as a license to spend whenever expenses come up. Instead, confidence comes from knowing the plan, not avoiding the purchase.

For that reason, projects with defined, fixed costs, a closed-end home equity loan may be the way to go. For ongoing projects with variable costs, a HELOC may be more appropriate.

For everyday spending or smaller purchases that will take less time to pay off, a credit card could be your best option.

Alignment Is the Real Mark of Responsibility

When you’re financing life upgrades, what does it mean to be “responsible”? Does it mean delaying purchases and timelines, or sacrificing things you want to cut costs?

No! Being responsible means aligning your project wants and timing with your income and financing strategies.

Now, will there be some things you have to sacrifice to fit your budget? Sure! But that doesn’t mean you have to keep costs as low as they can be at every turn.

If you’re renovating a room in your house, consider a slightly cheaper paint on the walls. Or, if you’re going on vacation, build some lower-cost meals into your plan.

You can still have things you want, just make sure you spend within your needs, even with flexible financing options.

The main thing to remember is that the right plan evolves as life does.

Conclusion: Permission Plus a Plan Changes Everything

When it comes to upgrading, you don’t have to choose between now and later. Financial planning can give you the confidence to move forward with your life upgrades, whether it be a home renovation, a vacation or a wedding.

When backed by intentional spending, upgrades feel lighter and you’ll avoid guilt or stress later.

When you’re ready to learn more, explore the related content below to learn more about the financial tools for upgrading your life.