Renovation Without Regret: Plan Your Financing

Learn the options, from home equity loans to credit cards.

Published Wednesday, July 1, 2026 to Advice

Your home is so much more than a residence. It’s a living thing.

Think about it… As your life evolves, so does your home.

Rooms change purposes when your family grows or when children grow up and move out. You make upgrades as styles change or as things wear out. And, sometimes, you renovate because you want to enjoy your home a little more.

Renovating can be exciting, but it often comes with stress. Uncertainty about project cost, or what it will limit later can both be big stressors.

When you start with a clear home renovation financing plan, you shift from reacting to costs to making confident decisions about your home.

In this guide:

- The importance of financing when renovating your home.

- Understanding the true cost of renovations.

- Comparing financing options.

- How to choose the right financing for your projects.

- What happens after the renovation.

Why Home Renovation Financing Matters

Renovations aren’t just construction projects that impact your home. They’re financial decisions that affect your future flexibility.

The stress of making design choices or choosing the right appliances fades once the decisions are made. But if you don’t think through the financing or how you’re going to pay for it, the stress could linger for years after you finish the project.

Considering financing early can help you establish a realistic budget before you start detailed planning. Because nothing is more deflating than scaling back after you’ve let yourself start dreaming.

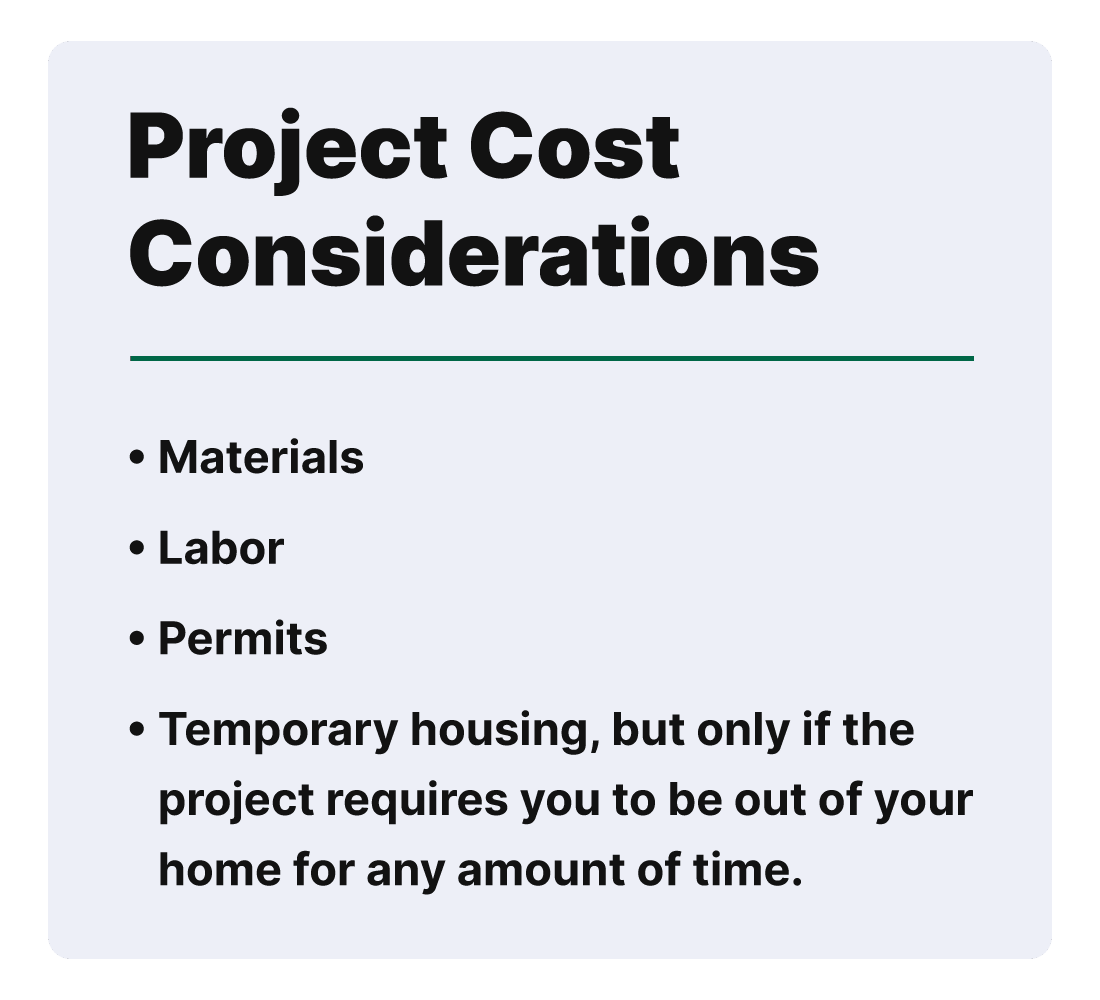

Step 1: Understand the True Cost of Your Renovation

Before you swing any hammers, the first thing you need to do is understand the full cost of your project.

Getting multiple quotes can help ensure you’re getting the best price on everything from labor to materials. If it’s a do-it-yourself project, price out all your items at multiple stores and shop around.

And when you’re setting your budget, be sure to set aside an extra 10% to 20% to account for surprises, unknowns and price changes.

Step 2: Decide on Home Renovation Financing

There is no shortage of ways to pay for home renovations and there’s no one right answer. If you're wondering how to finance home renovations, start by considering the following options:

- Pay with your savings

- Borrow with structured financing

- Use a combination of both

Paying with savings means no monthly payments, but you also reduce the amount you have on hand for when you need it for something else. Financing preserves your savings but requires monthly payments going forward.

When you use a combination of both, you can preserve some of your savings while keeping monthly financing payments manageable.

Step 3: Compare Your Home Renovation Financing Options

| Option | What is it? | Best for: |

|---|---|---|

| Savings | Cash you've set aside in a savings account, CD or other liquid account. | When you have enough cash on hand and don't want to make monthly payments or pay interest. |

| Closed-end home equity loan | A loan borrowed against the equity in your home. | When you know the exact cost up front. |

| Home equity line of credit (HELOC) | Similar to a closed-end home equity loan, but an open line of credit you can use as needed. | When costs may be flexible or you're doing your project in phases. |

| Home improvement loan | A special loan to be used specifically for home improvement projects. | You don't have equity or don't want to borrow against it. |

| Credit cards | A short-term financing account that is readily accepted online and in most stores. | Small projects when you don't want to pay closing costs on a home equity loan. Or to help you pay for odds and ends throughout a project. |

Closed-End Home Equity Loan

A home equity loan is a consumer-favorite for renovations. With a home equity loan, you can borrow against the equity in your home, which is the value of your home minus the remaining balance on your mortgage.

Learn more: see how home equity works and how to calculate yours >

With a closed-end home equity loan, you borrow one lump sum with a fixed rate and make fixed payments throughout your loan’s term. These are best when you know the exact costs up front and want to borrow exactly the right amount.

Many homeowners choose to use home equity for remodel projects because they have lower rates than most consumer loans and have flexible repayment options.

Home Equity Line of Credit (HELOC)

A home equity line of credit (HELOC) is almost the same as a closed-end home equity loan but with a few major differences. The biggest difference is that a HELOC is an open line of credit that can be used over and over again as needed.

With HELOCs, rates are usually variable, meaning they can change during your loan term. However, many HELOCs come with a fixed-rate period, usually 5 to 10 years.

A HELOC is great when you’re doing a project in phases, or don’t know exact costs up front. Borrow, renovate and repeat as needed!

Home Improvement Loan

Home improvement loans are more restrictive than home equity loans. They must be used for home repairs and renovations, but they don’t require you to have equity in your home.

Most options have a fixed rate and some allow you to borrow up to 100% (or more!) of your home’s value.

These are great when you don’t have equity in your home or don’t want to borrow against it.

Credit Cards

We all know what credit cards are, right? The little plastic things that let you spend money now and pay later?

Well, you can use those for home renovations as well. They aren’t ideal for larger projects because of the interest rate, but they are great for smaller purchases, like if you’re just getting new appliances or tackling a quick landscaping project.

The consideration is whether the project is big enough to justify paying closing costs on a home equity loan. If it’s not, credit cards may be the way to go.

Learn more tips for choosing the right credit card for your needs >

Savings and Planned Funds

What's the simplest way to pay for your home renovations? Cash!

Certificates of deposit (CDs) can help you set money aside for set period and earn a higher rate than a standard savings account. You can also use other accounts like a standard savings account or a money market.

This will help you avoid making monthly payments after the project is finished, but it also leaves you with less savings for something else in the future. So, consider carefully before paying for home renovations with savings.

Step 4: Match Your Financing to Your Project Timeline

Short-term projects and long-term projects require different financing. Same with projects that have fixed costs vs. variable costs.

A HELOC works well for long-term projects that evolve over time. For example, if you’re renovating your kitchen by yourself, you can break it up into phases and finance each phase as you go.

When your project is being done by a contractor all at once, and you know the total cost, a closed-end home equity loan is the way to go.

Credit cards can be used for all sorts of odds and ends throughout the process… as long as you stay on budget!

Step 5: Plan for What Happens After the Renovation

When the renovation is done, it’s time to relax and enjoy it. And that’s exactly why you need to plan ahead for the post-renovation financial impact.

Make sure you know what your monthly financing payment will be and that it fits your budget. Not stressing about the finances afterwards definitely helps you fully enjoy your home upgrades better long-term.

Also, check your credit report after the project is complete. Taking out new loans can impact your credit score, for better or worse and affect your ability to borrow for other things.

The key is balancing your need to improve your home while maintaining financial flexibility.

Common Mistakes That Lead to Renovation Regret

Some of the most common situations that lead to renovation regret are:

- Underestimating total cost, leading to higher monthly payments than you planned for.

- Choosing financing based only on rates. Remember, you need to match financing to your project.

- Overextending home equity. Since HELOC payments are a percentage of your balance, your payments get higher the more you borrow.

- Not planning for unexpected expenses. This can result in parts of the project being skipped for budgetary reasons, or higher monthly payments.

Frequently Asked Questions: Home Renovation Financing

How do I choose the right home renovation financing option?

Start by understanding your project size, timeline, and flexibility needs. If your costs are predictable, a fixed option may work best. If your timeline or costs may change, a more flexible option like a HELOC can help you adjust as you go.

Can I use home equity for a remodel?

Yes. You can use home equity through options like a home equity loan or a HELOC. Both allow you to borrow against your home’s value to help fund improvements.

Is a HELOC a good option for home renovation financing?

It can be a good fit for projects that happen in stages or have uncertain costs. A HELOC allows you to draw funds as needed instead of borrowing everything upfront.

Should I use savings or financing for my renovation?

It depends on your financial goals. Using savings can help you avoid interest, while financing can help you keep cash on hand for other needs. Many homeowners use a mix of both.

What is the biggest mistake to avoid when financing a renovation?

Underestimating the total cost. Always plan for extra expenses and choose a financing option that gives you some flexibility if costs change.

Conclusion: Build What You Want Without Second Guessing

Home renovations are an important investment, whether it’s for boosting your home’s value, or improving your comfort. When planned right with the right financing, you can get the job done without renovation regret.